The weight of unresolved tax debt does not stay in a filing cabinet. It follows you into sleep, into conversations with your spouse, into every piece of certified mail that lands in your box. If you are a business owner or self-employed professional in the Prescott area carrying IRS debt — or watching enforcement actions inch closer — understanding how tax resolution actually works is the first thing that changes your situation.

Before you can choose the right path forward, you need to understand what tax resolution is, what it is not, and what separates a firm that resolves root causes from one that just buys time.

Tax resolution is the process of negotiating with the IRS to reduce, restructure, or settle tax debt through formal programs — including penalty abatement, installment agreements, offer in compromise, and lien release. It is not a loophole. It is a structured, IRS-sanctioned process that requires documentation, strategy, and experienced representation to navigate correctly.

Key Takeaways

- The IRS has formal programs designed to reduce or restructure tax debt — but accessing them requires knowing which program fits your specific financial situation.

- Penalty and interest accrual does not pause while you wait. Every month without a resolution strategy is a month the balance grows.

- A CPA with tax resolution experience is not the same as a general CPA. Representation before the IRS requires specific knowledge of IRS collection procedures, negotiation protocols, and tax law.

- O’Neill Tax Resolution offers a free consultation — the fastest way to understand which resolution path applies to your situation before committing to anything.

- The most expensive mistake in tax resolution is waiting until enforcement actions (garnishments, levies, liens) are already in motion.

Why Does the IRS Feel So Impossible to Deal With Alone?

The IRS does not get emotional about collections. It just keeps moving.

The agency operates on automated systems that generate notices, escalate accounts, and initiate enforcement actions on a schedule — regardless of your circumstances, your intent, or your financial hardship. The bureaucratic momentum is the problem. It is not personal. But it is relentless.

Most people who end up in serious tax debt did not get there through negligence. A business hit a cash flow crisis. A divorce disrupted filing. A contractor misunderstood self-employment tax obligations for several years. The debt accumulated not from indifference but from a system that compounds faster than most people realize.

The root cause is almost never “I didn’t care.” It is almost always “I didn’t know what to do next, so I waited.”

And waiting is the mechanism by which manageable debt becomes crisis-level debt. The IRS charges both failure-to-pay penalties and interest simultaneously. According to IRS.gov, the current underpayment interest rate is set quarterly at the federal short-term rate plus 3 percentage points — and that accrues on top of penalties that can reach 25% of unpaid tax. The balance does not hold still.

What Does Tax Resolution Actually Include — and What Gets Resolved?

Tax resolution is not a single service. It is a category of IRS-sanctioned programs, each designed for a specific financial situation.

Here is how the primary resolution tools compare:

| Resolution Tool | Best For | What It Does | Realistic Timeline |

| Installment Agreement | Steady income, manageable debt | Structured monthly payment plan | 30–90 days to establish |

| Offer in Compromise | Significant financial hardship | Settles debt for less than owed | 12–24 months to resolve |

| Penalty Abatement | First-time or reasonable cause | Reduces or eliminates penalties | Weeks to months |

| Currently Not Collectible | Severe financial hardship | Temporarily halts IRS collection | Immediate, reviewed periodically |

| Lien Release / Subordination | Property or credit impact | Removes or reduces IRS lien | Varies by case complexity |

| Non-Filed Returns | Years of unfiled taxes | Brings accounts current | Depends on years involved |

The right tool depends on your income, assets, the age of the debt, and whether enforcement has already begun. This is not a checklist you work through on your own — it is a diagnostic process that an experienced CPA works through with you.

The resolution program that sounds most appealing is rarely the one that fits your actual financial picture. The one that fits your financial picture is the one that works.

Is an Offer in Compromise Actually Realistic for Most People?

This is where the most dangerous misconception lives.

National tax relief advertising has conditioned people to believe that “settling for pennies on the dollar” is a standard outcome. It is not. The IRS accepted roughly 13,000–16,000 Offers in Compromise annually in recent years, according to IRS data — out of millions of taxpayers with outstanding balances. Acceptance requires demonstrating that your Reasonable Collection Potential (RCP) — the IRS’s calculation of what they can realistically collect from your assets and future income — is less than what you owe.

Reasonable Collection Potential (RCP) is the IRS’s formula for determining the maximum amount they believe they can recover from a taxpayer, based on asset equity and projected future income. If your RCP is lower than your total tax debt, an OIC may be viable. If it is not, an OIC application wastes time and fees — and sometimes triggers faster enforcement.

This is a contrarian point worth sitting with: pursuing the wrong resolution strategy is not neutral. It can accelerate IRS action.

A practitioner with 35+ years of experience — like Patti O’Neill — does not start with the most appealing option. She starts with the most accurate picture of your financial situation and works backward to the strategy that the IRS will actually accept.

The O’Neill Tax Resolution Approach: What Makes It Different From a National Firm?

Most national tax resolution companies operate on volume. They assign cases to representatives who rotate, use templated strategies, and measure success by throughput. The relationship is transactional by design.

O’Neill Tax Resolution operates differently — and the mechanism behind that difference matters.

Patti O’Neill is a CPA with a Master’s degree in Taxation and more than 35 years of hands-on tax resolution experience. She has built long-term relationships with clients — some spanning 20+ years — because her approach treats the tax problem as a symptom of a larger financial picture that needs to be understood, not just processed.

Tax problems are rarely just tax problems. They are the visible edge of a financial situation that needs to be understood before it can be resolved.

That framing changes the work. Instead of matching your case to a template, O’Neill Tax Resolution builds a custom plan — one that addresses the root cause of the debt, not just the current IRS notice on your desk.

A concrete example: a self-employed contractor came to O’Neill Tax Resolution three years into penalty accrual with a balance that had grown significantly beyond the original tax owed. Through a combination of penalty abatement (qualifying under reasonable cause), a structured installment agreement, and amended filings that corrected prior-year errors, the total liability was reduced substantially and resolved within 11 months. The enforcement actions that had been initiated — including a wage levy — were released within the first 60 days of representation. To understand how O’Neill Tax Resolution actually works in practice, that diagnostic process is the method behind every outcome.

That outcome was not the result of a single program. It was the result of a diagnostic process that identified every available lever.

What Are the Real Limitations of Tax Resolution Services?

Honest answer: tax resolution is not a solution for everyone, and a firm worth trusting will tell you that directly.

Tax resolution does not work when:

- The taxpayer is unwilling to provide complete financial documentation. The IRS requires full disclosure; incomplete information produces incomplete results.

- The debt is very recent and enforcement has not yet begun. In some cases, the most effective strategy is simply filing correctly and paying — not engaging a resolution process.

- The taxpayer has significant assets and income that make hardship-based programs inapplicable. An OIC or Currently Not Collectible status requires genuine financial hardship — not just a preference to pay less.

- Criminal tax fraud is involved. Resolution services address civil tax matters; criminal exposure requires a tax attorney, not a CPA.

O’Neill Tax Resolution will tell you which category you fall into during the free consultation. That clarity — even if the answer is “you don’t need a resolution firm” — is itself a service. For Arizona taxpayers weighing their choices, an honest comparison of tax resolution versus the alternatives can help clarify which path makes the most sense before that conversation begins.

Who Should Not Wait Another Month to Get a Professional Assessment?

If any of the following are true, the cost of waiting is measurable and real:

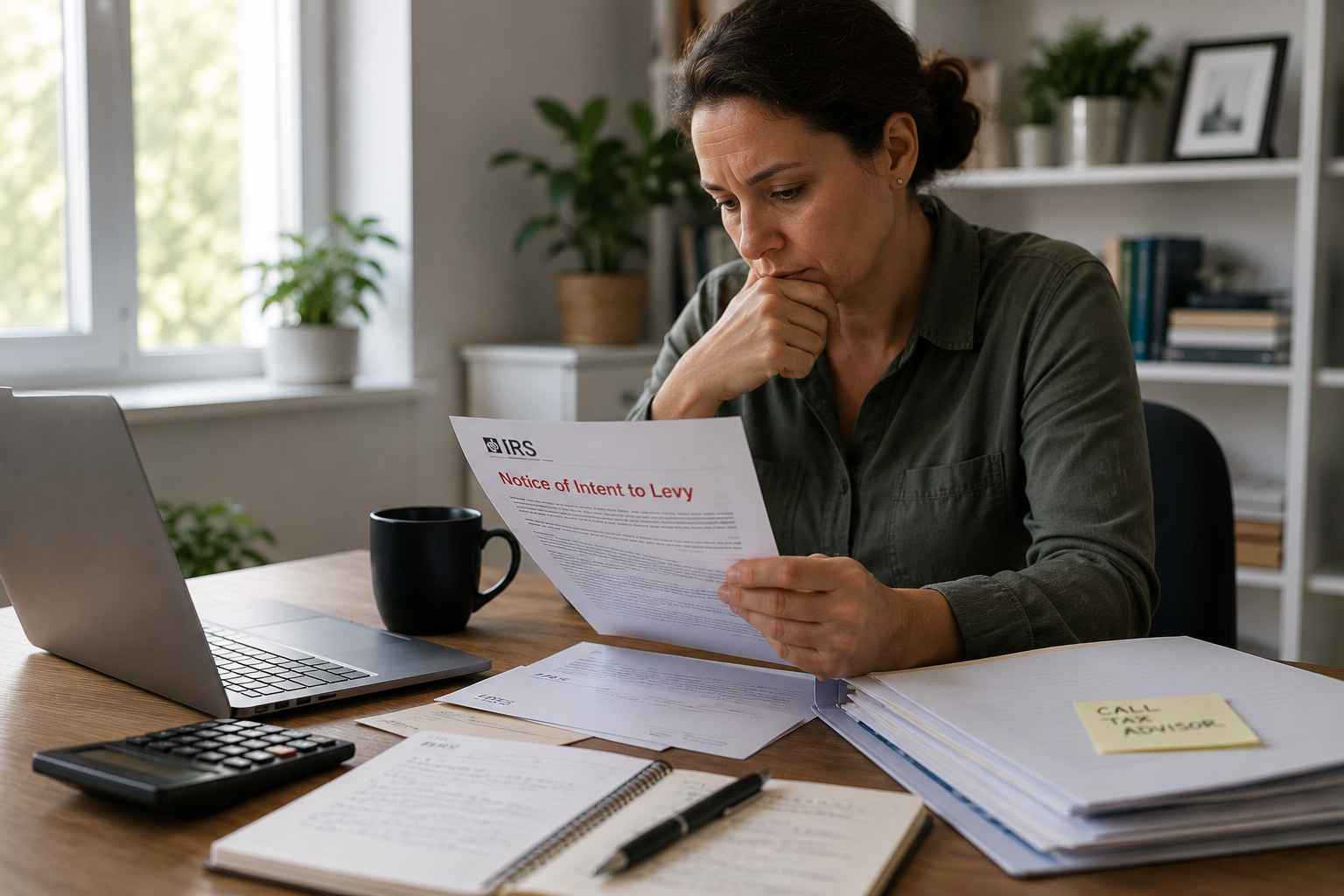

- You have received an IRS Notice of Intent to Levy (CP504 or LT11)

- You have unfiled returns for two or more years

- You are a business owner with unpaid payroll taxes (Trust Fund liability)

- You have received notice of an IRS lien filed against your property

- Your balance has grown past the point where you could realistically self-resolve

The single most expensive decision in tax resolution is the decision to wait one more month.

Not because of fees. Because of compounding. Every month of inaction is a month of penalty accrual, interest accumulation, and narrowing options.

Frequently Asked Questions

How do I know if I actually qualify for an offer in compromise or if it’s just a sales pitch? The IRS uses a specific formula called Reasonable Collection Potential to evaluate OIC applications. If your assets and projected income exceed what you owe, the IRS will reject the offer. A qualified CPA can calculate your RCP before you apply — so you know whether the strategy is viable or whether a different approach fits better.

What happens if I just ignore the IRS notices and hope it goes away? Ignoring IRS notices does not pause the process — it accelerates it. The IRS follows a structured escalation sequence that moves from notices to liens, then to levies on wages and bank accounts. The longer the account sits unaddressed, the fewer resolution options remain available.

Can a CPA really negotiate with the IRS on my behalf, or do I need a tax attorney? A CPA with an active Enrolled Agent status or CPA license can represent you before the IRS in all collection and audit matters. You need a tax attorney specifically if there is potential criminal tax liability. For the vast majority of tax debt and audit situations, an experienced CPA like Patti O’Neill is fully authorized and often more effective.

How long does tax resolution actually take from start to finish? It depends on the resolution path. A penalty abatement request can resolve in weeks. An installment agreement typically takes 30–90 days to establish. An Offer in Compromise can take 12–24 months from submission to IRS decision. The timeline is set largely by the IRS — but having a qualified representative means the process moves without stalling.

What does a free consultation with O’Neill Tax Resolution actually cover? The consultation is a diagnostic conversation — not a sales call. Patti O’Neill reviews your situation, identifies which IRS programs apply, and gives you an honest assessment of your options and realistic outcomes. You leave with clarity about your situation whether or not you decide to engage the firm.

I filed late for several years. Is it too late to fix that? Non-filed returns are one of the most common issues O’Neill Tax Resolution resolves. Filing late is always better than not filing — and in many cases, getting current on filings opens access to resolution programs that are otherwise unavailable. The IRS cannot negotiate with a taxpayer who is not in compliance.

Will hiring a tax resolution firm make the IRS more aggressive toward me? No — and this is a common fear worth addressing directly. Engaging professional representation signals to the IRS that you are taking the debt seriously and working toward resolution. It typically results in communication being redirected to your representative, which reduces direct IRS contact and often slows enforcement while a resolution is being negotiated.

The Decision You Are Actually Making Right Now

If you have read this far, you are not looking for a loophole. You are looking for a way out of a situation that has been taking up space in your life for too long.

The next step is not a commitment. It is a conversation.

Call O’Neill Tax Resolution at 928-378-8490 and schedule your free consultation with Patti O’Neill. Come with your most recent IRS notice, a rough sense of what years are involved, and the willingness to be honest about your financial picture. You will leave that conversation knowing exactly where you stand — and what resolving this actually looks like for your specific situation.

That clarity is the first thing that changes. Everything else follows from it.

References

IRS.gov — Official source for current underpayment interest rates, Offer in Compromise acceptance data, and IRS collection procedures including Notice CP504 and LT11 escalation sequences.

IRS — Annual Data Book, published yearly, covering statistics on Offer in Compromise submissions and acceptances.